Equity Portfolio

Overview

To outperform inflation.

Actively managed with a long-term bias to equities. The Portfolio normally invests in a wide range of ETFs to gain significant diversification and exceptional liquidity at very low cost. The portfolio follows the same equity allocation as the SCM Long-Term Return (GBP).

| Stock Short Name | Percentage of Portfolio |

|---|---|

| iShares Core MSCI EM IMI UCITS ETF | 20.8 |

| Amundi UK Equity All Cap UCITS ETF | 17.1 |

| iShares Core FTSE 100 UCITS ETF | 15.4 |

| Amundi MSCI Japan UCITS ETF | 9.2 |

| Vanguard FTSE 250 UCITS ETF | 7.1 |

| Invesco FTSE RAFI US 1000 UCITS ETF | 6.5 |

| WisdomTree US Quality Dividend Growth UCITS ETF | 6.4 |

| SPDR MSCI EM Small Cap UCITS ETF | 6.3 |

| iShares Core MSCI EMU UCITS ETF | 4.9 |

| WisdomTree Japan Equity UCITS ETF | 3 |

| Number of Holdings | Best Dividend Yield Forward 12m | Best Price to Book Forward | Best P/E Ratio | Best LTG EPS |

|---|---|---|---|---|

| 5,976 | 3.1% | 1.9 | 14.4 | 12.5% |

| Equity | 9.9% |

|---|---|

| Asia Pacific Ex. Japan (MSCI Asia Ex Jap) | 19.0% |

| Em Markets (MSCI EM) | 17.9% |

| Japan (MSCI Japan) | 14.5% |

| US Equities (MSCI USA) | 13.2% |

| Europe Excl UK (MSCI Eur. Ex UK) | 11.4% |

| UK Equities (MSCI UK) | 9.7% |

| UK Index-Linked Gilts (Barclays UK Infl Linked) | 8.9% |

| UK Gilts (Bloomberg UK Govt All>1 Yr) | 6.9% |

| UK Corp Bonds (iBoxx Large Cap TRI Index) | 5.2% |

Performance is based on the monthly performance of the first client discretionary portfolio after all charges. Individual client portfolios may differ due partly to differences in the timing of initial investment or withdrawals or rebalancing. Competitor data is based on the average performance of the IA Global Mixed Bond and the IA Mixed Investment 40-85% Shares Sectors and the comparison is offered as a guide only.

| 12m to 31/05/2021 | 12m to 31/05/2022 | 12m to 31/05/2023 | 12m to 31/05/2024 | 12m to 31/05/2025 | 12m to 31/05/2026 |

|---|---|---|---|---|---|

| 29.1% | 0.6% | -1.4% | 15.3% | 6.3% | 28.4% |

Source: SCM Private LLP

Past performance is not a guide to future returns. The value of investments and the income from them can go down as well as up, so investors may not recover the amount of their original investment.

| ALL Fees & Charges | Percentage |

|---|---|

| SCM Discretionary Fund Management Charge | 0.40% |

| Underlying ETF costs (KIID Ongoing Charge) | 0.19% |

| Transaction Costs of buying/selling funds | 0.12% |

| Transaction Costs within funds | 0.06% |

| Custody & Administration Fee | 0.12% |

| Total Fees & Charges | 0.89% |

In May, we rebalanced all the MoneyShe/SCM Portfolios, completing the rotation into UK government bonds that we began in the Spring – a move made when gilt headlines were at their most alarming, and one that proved well-timed.

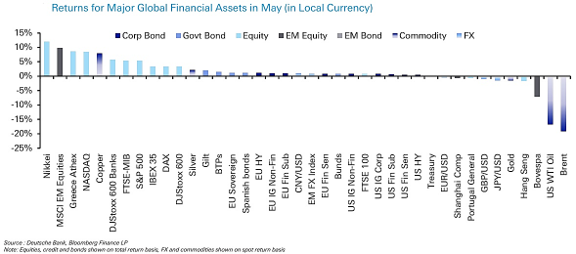

May was a risk-on month as hopes of a US-Iran deal firmed. Brent crude fell 19.3%, its biggest monthly decline since 2020, to around $92 a barrel, and with it, fears of stagflation receded. The S&P 500 rose 5.3% in total-return terms to a record high, the STOXX 600 gained 3.2%, and the Nikkei gained 11.9%.

The most speculative areas led: the Philadelphia semiconductor index rose 22.2%, and South Korea’s KOSPI 28.5% (up 102.4% this year). Sovereign bonds recovered towards the month-end as inflation worries eased.

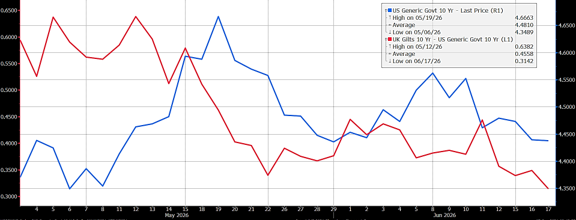

UK gilts: not believing the headlines

In mid-May, UK gilts were friendless. On 15 May, the 10-year yield hit a post-2008 high of 5.17% amid Labour’s local-election losses, ministerial resignations, and doubts over the fiscal rules. We judged the pessimism overdone and a yield above 5% to be good value. The May rebalance completed our build-out across short, conventional, and long maturities. Within days, gilts rallied: the 10-year closed at 4.81%, and gilts returned around 2.0% for the month. As the chart below shows, UK gilt yields fell substantially, and the premium of UK gilt yields over US government yields also declined. The SCM Ethical (ESG) Portfolio holds no government bonds, meeting its fixed-income exposure through screened corporate and ultra-short holdings.

Don’t be too relaxed about inflation

We caution against assuming oil-driven inflation will fade quickly. US headline CPI has risen above 4% for the first time in three years. The Federal Reserve’s stickier “supercore” measures are rising, and the NFIB small-business price index is at its highest level since 1981. UK inflation figures released this morning showed CPI was steady at 2.8% in the year to May, but services inflation picked up to 3.6%, a reminder that the stickier components have yet to ease. With Kevin Warsh chairing his first meeting and markets no longer expecting rate cuts, the risks remain skewed to the upside. Our focus on genuine diversification and on buying bonds at attractive yields is designed to help portfolios withstand that environment.

The insanity of SpaceX

If gilts were a study in excessive pessimism, SpaceX is the opposite. After May’s successful Starship maiden flight and Starlink price rises, it floated in mid-June in the largest listing in history and was soon valued at around $2.75 trillion. Alongside semiconductors, up by more than a fifth in a month, this shows how much optimism is embedded in the most fashionable assets, which are already volatile, with the Nasdaq 100 down around 7% from its peak and Oracle around 25%. We make no judgments about technology, but we stay broadly diversified rather than concentrating on a handful of fashionable names.

MoneyShe/SCM Portfolios

May was a strong month and a welcome contrast to early Spring. Broad international equity exposure captured the global rally, and the gilt positioning boosted returns. We continue to hold no gold, which fell for a third consecutive month.

We remain focused on capital preservation, valuation discipline and global diversification, and continue to monitor developments very closely.

Alan Miller, Chief Investment Officer

17 June 2026