It’s that time of year again — wedding bells are ringing, save-the-dates are landing on the fridge, and hope, dreams and joy for the future overflow. Whether the diamond is on your finger or your best friend’s, this season makes us dream bigger than ever. Let’s match that energy with something just as powerful: a plan for your financial future. In this post, we’ll explore Love, Marriage & Money – MoneyShe Blog and how these themes come together to help you shape a confident financial path.

By the time you say “I do,” you’ve probably argued over flowers, agonised over seating plans, and rewritten your vows three times. But have you sat down and had an honest conversation about money? If the answer is ‘not really’, you’re not alone. And it’s time to change that.

Marriage is an act of love and commitment, but it is also one of the biggest legal and financial contracts you will ever sign. The most romantic thing you can do is plan for both the magic and the maths. Wishing for a life of bliss is beautiful — building one that holds firm whatever comes is powerful.

The Numbers Behind the Big Day

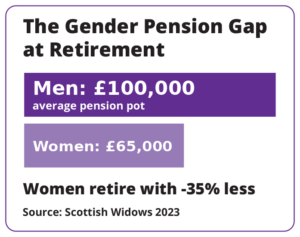

Let’s start with honesty. Roughly 42% of marriages in England and Wales eventually end in divorce (ONS). The average UK wedding now tops £20,700 (Hitched Wedding Report). Yet a survey found 1 in 5 women don’t know their partner’s salary. And the gender pension gap still hovers around 35%, meaning women typically retire with a third less than men.

Add this to the picture: money is the number one issue married couples argue about, and the second leading cause of divorce after infidelity (Ramsey Solutions). Talking about money isn’t optional — it’s protective.

This isn’t doom. It’s data. And data is power.

Figure 1: The pension pot gap at retirement.

Step 1: Have the Money Conversation

Before the rings, schedule what I call a Money Date. Open the wine, open the spreadsheets. Cover:

- Income, savings, debts, and credit scores — no surprise balances surfacing after the honeymoon

- Spending styles — saver, spender, or somewhere in between

- Money personalities — most couples have one ‘numbers nerd’ and one ‘free spirit’. Both voices matter; neither gets to opt out of the budget

- Big goals (home, children, career breaks, travel) — and realistic timeframes. There is no rule that says you must own a home, start a family, or honeymoon in Bali in year one

- Whether a prenup or cohabitation agreement makes sense

A prenup is not a lack of trust. It is a love letter to your future selves — clarity today prevents conflict later.

Step 2: The Three-Account Method

The healthiest couples we work with use what we call the “Yours, Mine & Ours” structure:

- A joint account covers shared bills proportionally to income — because whoever earns more doesn’t get more votes. Income is not authority.

- A personal account protects autonomy — no one should ask permission to buy a birthday gift for their mum, give to charity or have a spa day.

- A long-term wealth account (ISA, SIPP, GIA investment account) is yours alone, growing quietly in the background.

One important caveat: separate accounts are about autonomy, not secrecy. Hidden credit cards, undeclared debts and stash-it-and-hope savings are financial infidelity — and they erode trust as fast as any other kind. Transparency about the whole picture is non-negotiable; how you organise it after that is up to you.

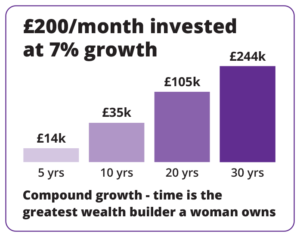

Step 3: Invest Like Your Future Depends On It (Because It Does)

Here’s a stat that should be in every bridal magazine: women who invest outperform men by an average of 0.4% per year. We just invest less often. Don’t leave your savings idling in a current account, losing to inflation. Open a Stocks & Shares ISA — £20,000 annual allowance, tax-free growth.

Figure 2: Compound growth — time is the greatest wealth-builder a woman owns.

Step 4: Mind Your Pension Gap

If you take a career break for children, your pension contributions often stop — but your retirement doesn’t. Keep paying in, whatever you can afford — don’t put yourself last, put yourself first — even £100 to £200 a month.

Ask your partner to contribute to your pension during career breaks; it’s a simple conversation that can be worth tens of thousands by retirement. Claim Child Benefit (even if you have to repay it) so you keep your National Insurance credits towards the State Pension. And remember, pensions are usually shared assets in divorce — know what’s yours and never sign anything without independent advice.

Illness, redundancy, parenthood, widowhood, or simply a change of heart — none of these should leave you starting from zero.

A financially resilient woman doesn’t expect the worst. She prepares for everything — so she’s free to fully enjoy the best.

|

Financial resilience isn’t about expecting the marriage to fail. It’s about knowing that you, the woman walking down the aisle, will be okay no matter what life delivers. |