MoneyShe — Market Insight

An investor recently asked us a very pertinent question. With a queue of huge companies — SpaceX among them — lining up to float, and the rules for getting into the big stock-market indices being loosened, could our portfolios get dragged into an over-priced bubble? And what on earth is going on with “tokenised” shares? Here’s the answer, in plain English.

What’s changing, and why it matters

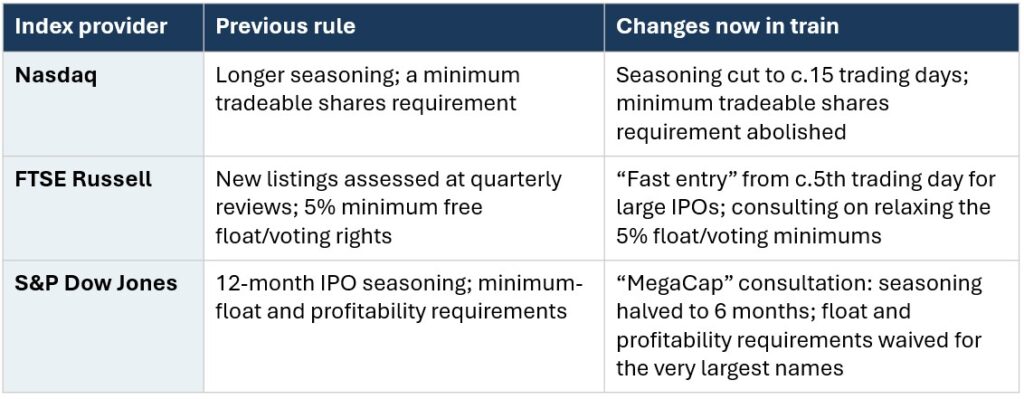

Stock-market indices (like the ones many “tracker” funds follow) used to require new companies to wait and prove themselves before admitting them. Those guardrails are being relaxed, just as some giant companies prepare to list. Here’s the short version:

The worry is simply explained. An ordinary tracker fund must buy a company once it joins the index — at whatever the price happens to be, even if that price has been bid up to silly levels. As one expert put it: if a stock doubles the week after listing, the tracker still has to buy it. It can’t say no.

Why does your money in a MoneyShe portfolio work differently?

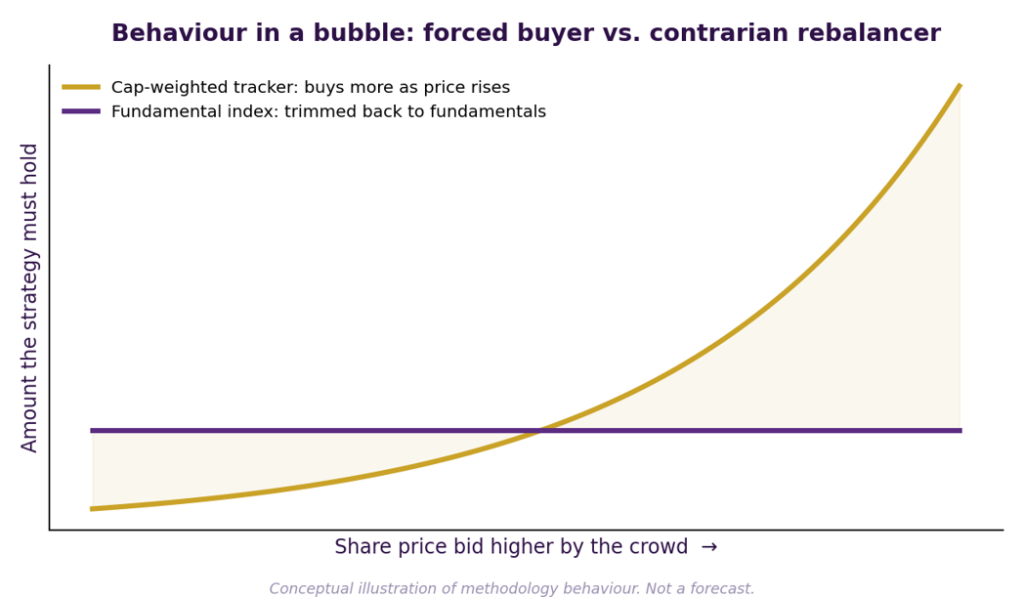

Here’s the key. A normal tracker decides how much of each company to own based on its share price — so the more excited the crowd gets, the more the fund is forced to pile in. The fund we use for US shares does the opposite.

It sizes each company by how big and real the business actually is — its sales, its cash flow, its book value, and the dividends it pays. The share price doesn’t get a vote.

In a bubble, an ordinary tracker is forced to keep buying as the price climbs. Our approach trims back to what the business is worth.

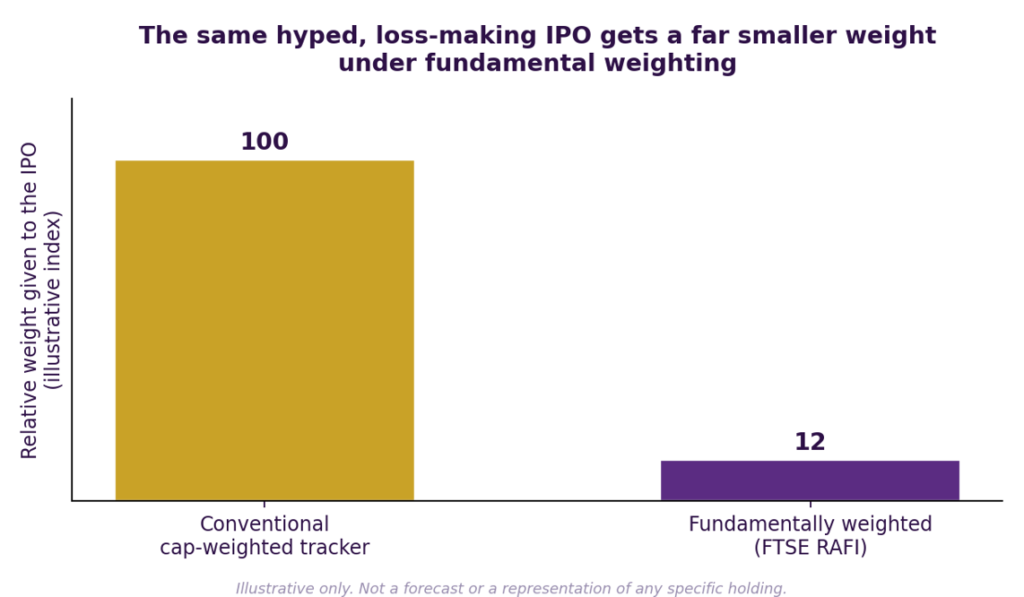

Take SpaceX. It’s reportedly listing at around 100 times its sales, lost about $4.9bn last year, and pays no dividend. To a normal tracker chasing share prices, that could mean a big holding. Our approach — which looks at the real business — sees it as tiny. So, we simply aren’t forced to buy a lot of it at an inflated price.

How much of a hyped new company you’d own: a normal tracker (large) versus our approach (small). Illustrative.

There’s a nice bonus, too: once a year, our fund quietly trims the companies whose prices have run too far ahead and tops up the ones left behind. It goes against the hype instead of chasing it. And for our balanced portfolios, we’re never forced to be fully invested – if markets get choppy, we can hold more cash and steadier assets.

Will all these new listings crash the market? MoneyShe views: not straight away

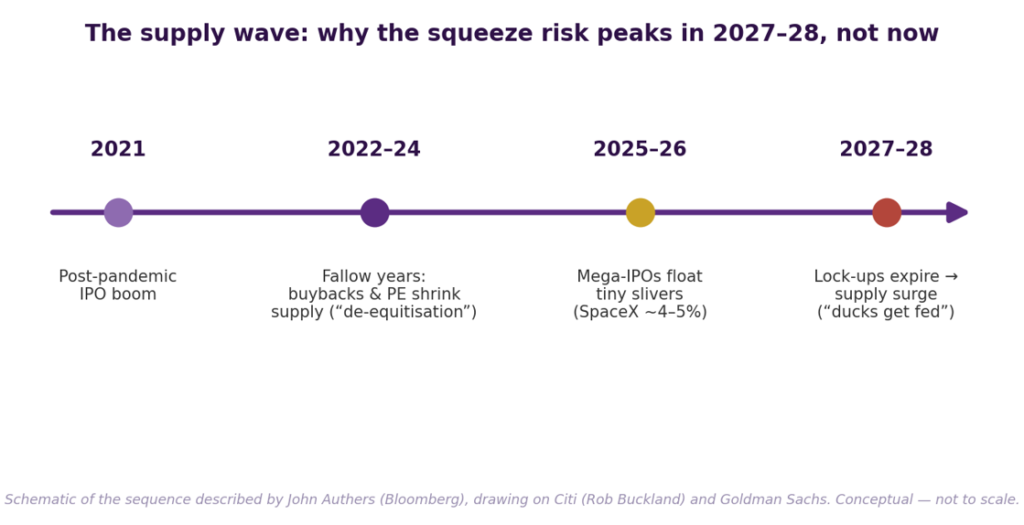

There’s a bigger worry doing the rounds: if SpaceX, OpenAI, Anthropic and others all list at once — and Alphabet (Google’s parent) alone wants to raise about $80bn — won’t all that new stock drag the whole market down? Bloomberg’s John Authers lays it out clearly, and the short answer is probably not right away, but the pressure builds over time.

Why not right away? For years, the market has been shrinking, not growing. Companies have been buying back their own shares and going private faster than new ones have been floated. (The clunky word for it is “de-equitisation”.) A few thin slivers of SpaceX and friends won’t flip that overnight.

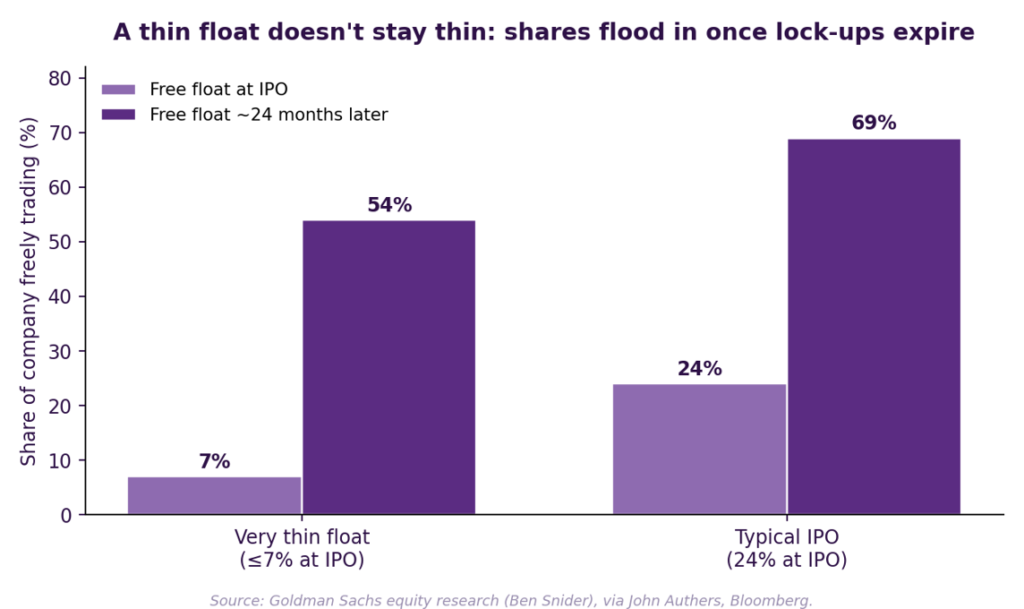

The catch is what happens later. A company that floats only a tiny piece of itself doesn’t stay that way. Goldman Sachs found that firms listing 7% or less of their shares had 54% trading within two years; a more typical 24% grew to 69%. Once the founders’ “lock-up” periods end, all that held-back stock hits the market.

A thin float doesn’t stay thin: how much of a company is freely trading about two years after listing. Source: Goldman Sachs, via John Authers, Bloomberg.

That’s exactly what happened after the dot-com peak in 1999. The crash came in 2000 as lock-ups expired and founders cashed out. So, the squeeze, if it comes, is more likely around 2027–28 than today.

Thin floats now, a heavier wave of shares as lock-ups expire later. A simple schematic, after John Authers (Bloomberg). Conceptual — not to scale.

What does that mean for you? Two things you already have if you are a MoneyShe client. Because our US fund weights companies by real size, not share price, we’re never forced to pile into these names at silly prices on day one. And because we can adjust how much you hold in shares versus safer assets, we can ease off if markets get wobbly, rather than being dragged down with the crowd. (It’s also worth knowing that founders like Elon Musk plan to keep nearly all the control – new investors will just be coming along for the ride.)

And those “tokenised” shares?

“Tokenisation” just means turning a share or asset into a digital token recorded on a blockchain. Done properly, it can make buying and selling faster and cheaper. The problem is the sales pitch.

Some tokens are marketed as “backed” by property or by stakes in exciting companies, but the backing is hard to value, hard to sell, or not really there. Regulators recently acted against Unicoin (see the SEC’s enforcement action), a firm that boasted of “$3 billion in sales” when its own accounts showed it had raised maybe $110m. New technology, very old trick.

The good news is that your money goes nowhere near this. At MoneyShe, we invest only in regulated, listed, easy-to-sell investments, such as mainstream funds. No crypto tokens, no “pre-IPO” tokens, no “asset-backed” digital currencies. We keep an eye on these trends, but they’re kept well away from your savings.

In one sentence

The risks in the headlines are real, but they hit funds that are forced to chase rising prices; yours is built to follow the real value of real businesses, with the freedom to play it safe when markets wobble.

The MoneyShe Investment Team

Important information

The value of investments can go down as well as up, so you could get back less than you invest. Past performance is not a guide to future returns. MoneyShe is a trading brand of SCM Private and does not give personal advice based on your circumstances. We aim to provide understandable information so investors can make fully informed decisions. If you are unsure about the suitability of our portfolios, please contact an independent financial adviser. Third-party data and commentary (including from Bloomberg, Goldman Sachs and the Financial Times) are cited in good faith; charts marked “illustrative” or “conceptual” are schematic and are not forecasts or representations of any specific holding. SCM Private LLP, authorised and regulated by the Financial Conduct Authority (No. 497525).