A MoneyShe take on the Pensions Commission’s May 2026 report – and a plan for a comfortable future.

Let’s start with the headline

Last week, the Pensions Commission, the independent group of experts the Government asked to look into how Britain is saving for retirement, told us something we already knew but most of us would rather not think about:

Around 15 million people in the UK are not saving enough to retire comfortably. If nothing changes, that number heads towards 19 million.

As one expert bluntly said, “We are already in a pensions crisis.” We agree. And if you are a woman reading this, the news is even more uncomfortable: the gap is bigger, starts earlier and lasts longer for you.

This blog is focused on two things:

- Explaining, in plain English, what the report says.

- Give you a five-step checklist you can start working through today.

Stay with us. The numbers are heavy, but the plan really isn’t.

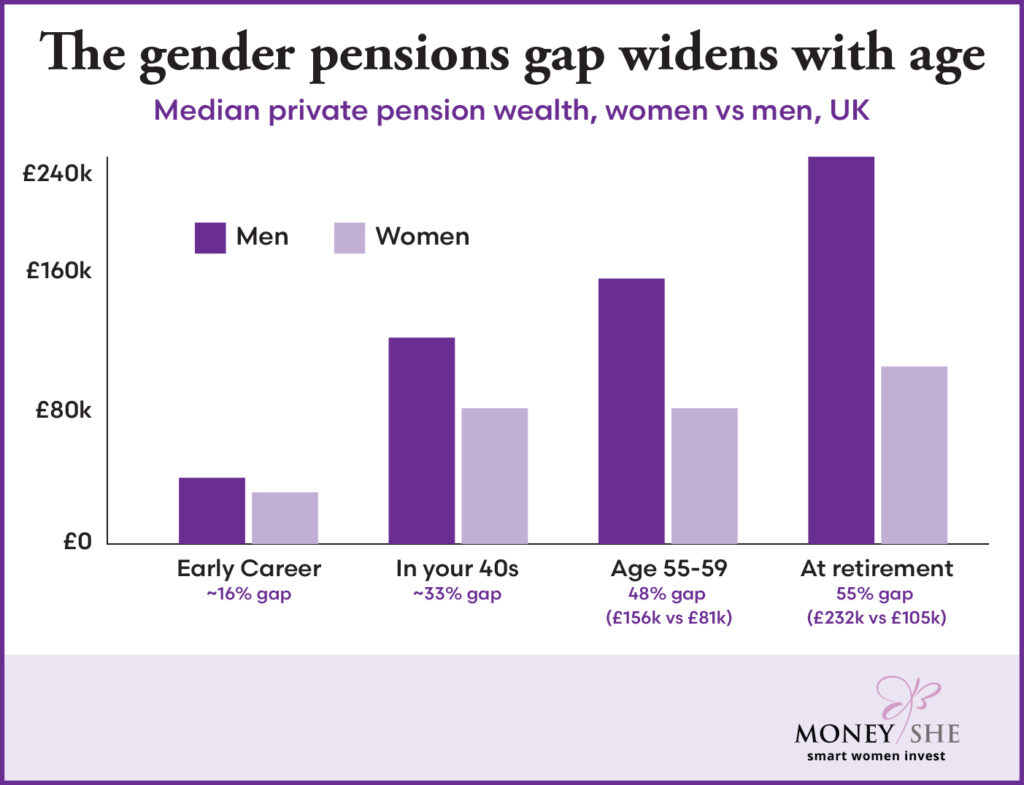

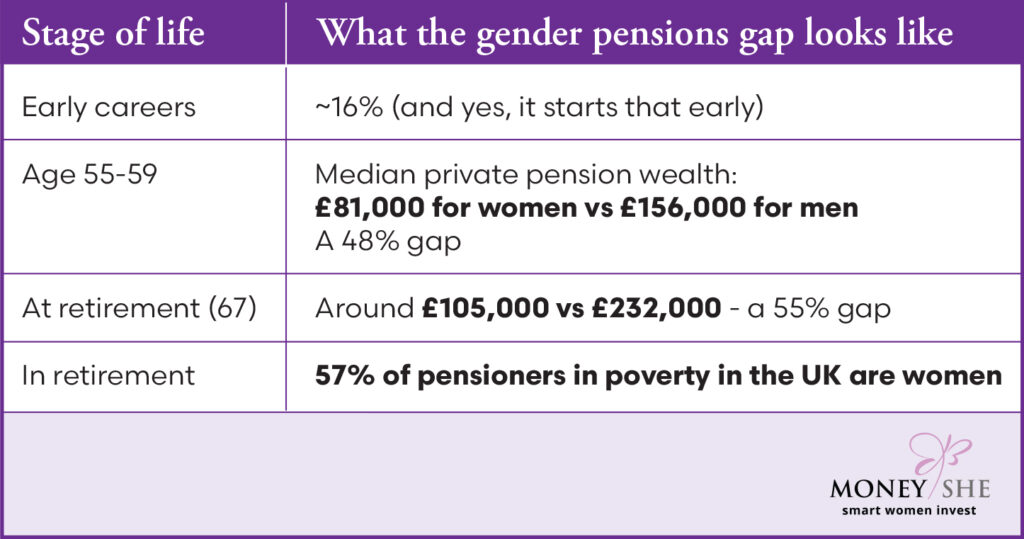

Why are women paying for this crisis twice

The Pensions Commission flagged women, carers, the self-employed and many ethnic minority savers as the groups hit hardest. Here is what the broader UK data is telling us.

Why? Because the pension system was designed around an uninterrupted, full-time, well-paid male career. The minute your working life doesn’t look like that – because you took maternity leave, dropped to part-time when the kids were small, looked after an elderly parent, freelanced, retrained, or had a few years between jobs – the system stops working for you.

Auto-enrolment helped. It got millions of women into a workplace pension for the first time. But the £10,000 earnings trigger still excludes huge numbers of women in part-time roles, and the standard 8% contribution rate was never going to be enough for someone who’d also spent years out of the workforce.

In other words: it’s not you. It’s the system design. MoneyShe has been shouting this – and the Pensions Commission has finally agreed and said it out loud.

The four numbers from the report you need to know

You don’t need to read all 200+ pages. But these four numbers carry most of the weight.

- 15 million. People in the UK are under saving for retirement right now.

- 8%. The minimum amount most workplace pensions automatically save (employee + employer combined). Almost everyone treats this as “the right amount.” It isn’t!

- 4%. The share of self-employed people paying into a pension. If you’re freelance, contracting or running your own business, the system is almost entirely opt-in. Nobody is opting you in.

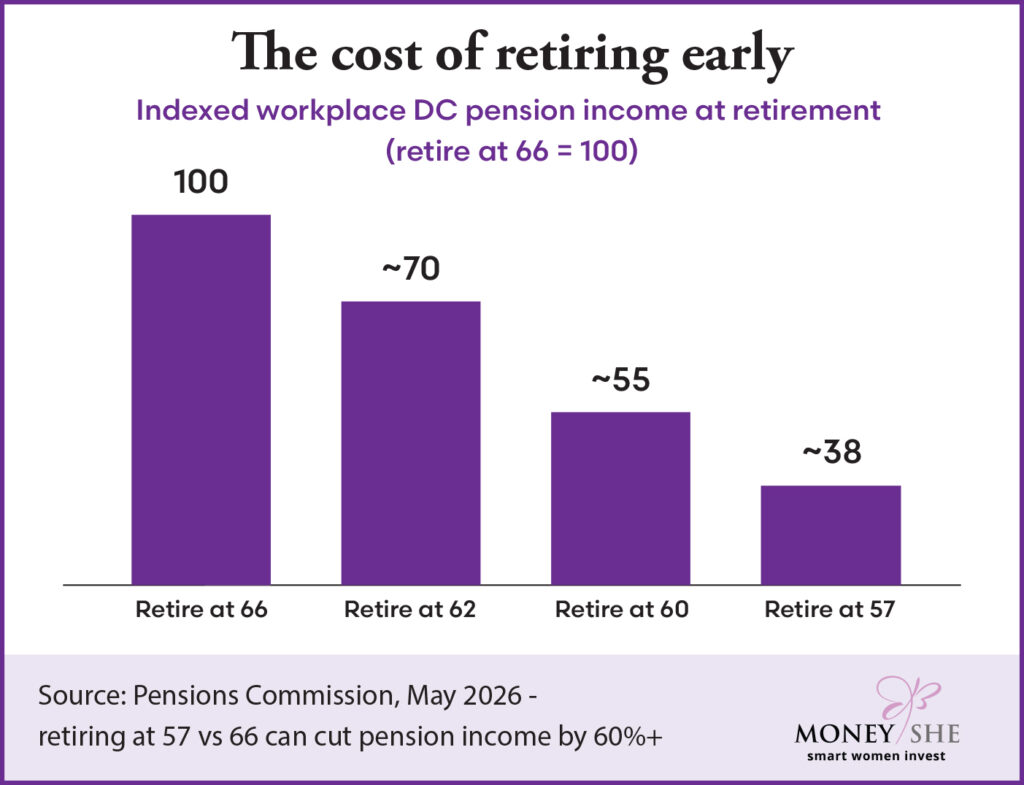

- 60%+. How much workplace pension income can you lose by retiring at 57 instead of 66? Early retirement is brilliant, but it is expensive, and the cost is invisible until it’s too late.

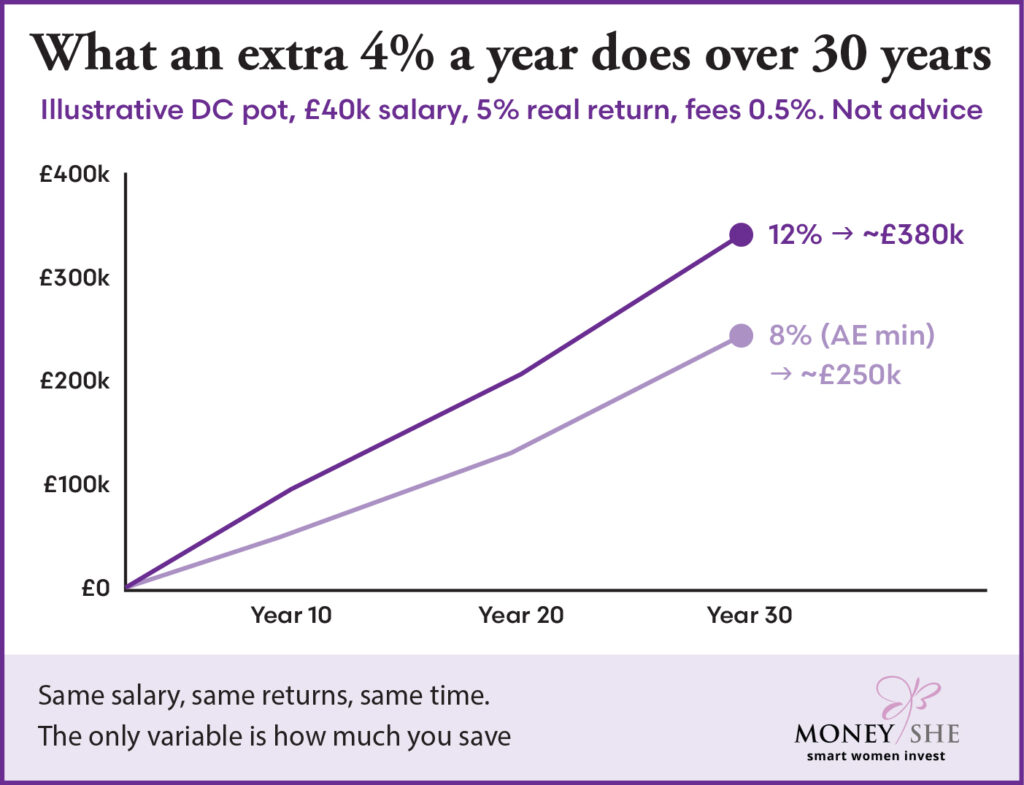

“But I am saving 8%. Surely that’s fine?”

Here’s a chart that helps our clients understand what we’re talking about.

Same person, same salary, same investment returns, same 30 years. The only difference is that you contribute 12% instead of 8%.

The bigger pot is roughly 50% larger. That’s the difference between “I can manage” and “I have choices.”

You can’t predict the markets, geopolitics, or the FTSE, but the very good news is that this is the part you can control – you can decide what comes out of your income and goes into your pension pot.

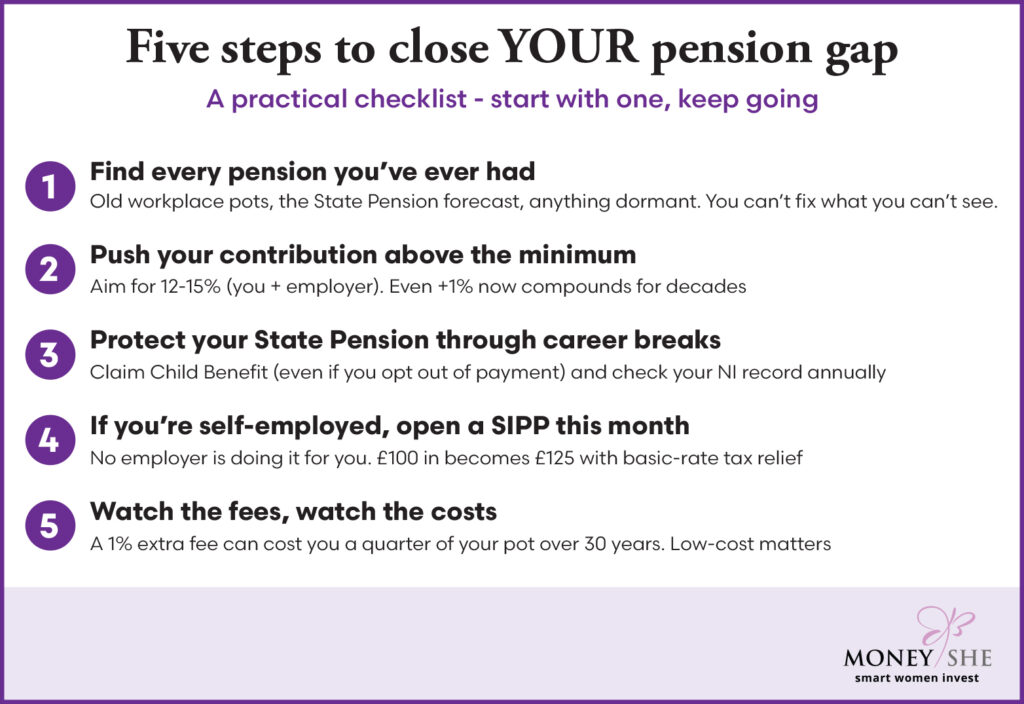

Your five-step plan – start today, reduce your stress tomorrow

Step 1 – Find every pension you’ve ever had

Most women in their 40s have at least three. Old workplace schemes. A personal pension from a previous job. Maybe a SIPP you started and forgot about.

- Check the Pension Tracing Service.

- Get your State Pension forecast.

- Make a single list with provider, current value, and contribution rate.

You can’t close a gap you can’t see.

Step 2 – Push your contribution above the minimum

Pick a target – 12% to 15% combined (you + employer) is a sensible aim. Then move in that direction in small, affordable steps.

- See if your employer will match higher contributions. Many will, and you’re leaving money on the table by not asking.

- Use salary sacrifice if available – more goes in, less tax leaves your payslip.

- If you get a pay rise, redirect part of it to your pension before it gets swallowed up.

Step 3 – Protect your State Pension through every career break

The State Pension is more valuable than people realise. To get a full one, you need around 35 qualifying years of National Insurance. Career breaks can quietly leave gaps.

- If you’re a parent claiming Child Benefit (even if your partner earns too much and you’ve opted out of the payment), claim it on paper – it gives you NI credits.

- Look after a grandchild regularly while their parents work? You may be entitled to Specified Adult Childcare Credits.

- Check your NI record at gov.uk/check-national-insurance-record. Gaps from the last few years can often be filled cheaply.

Step 4 – If you’re self-employed, open a SIPP, sooner not later

The single biggest blind spot in the report. If your income is self-employed, there is no employer setting up a pension for you. There is no nudge, no opt-out form, no default. You have to do it on purpose.

The good news: a low-cost SIPP (Self-Invested Personal Pension) is built for exactly this. You choose how much, when, and where it’s invested. Every £80 you put in becomes £100 thanks to basic-rate tax relief. Higher- and additional-rate taxpayers can claim more back through self-assessment.

Even £100 a month, started today, makes for a more comfortable retirement.

Step 5 – Watch the fees

A 1% extra in annual fees can quietly cost you around a quarter of your pot over 30 years. This is the single most underrated lever in retirement saving.

When you compare pensions, ask:

- Platform fee?

- Fund/investment fees (the OCF/TER)?

- Transaction costs?

- Any adviser or service charge?

Add them up. If it’s much over 1% all-in for a simple portfolio, ask why.

Deeds not words

It’s tempting to read all of this and feel a bit defeated. Please don’t. The Pensions Commission’s report isn’t really bad news – it’s permission to take this seriously, in public, without feeling guilty or that you’re alone in this. The 15 million figure is so large precisely because this is a system-wide problem, not a personal failure.

The women we hear from at MoneyShe don’t need to be told the system is broken. What they need is explanations, education and executable solutions – no jargon, no blame. Just choices.

Ready to take action?

If you’d like a low-cost, transparent SIPP run by people who genuinely care about closing the gender pensions gap, and who are invested alongside you – that’s exactly why we’ve built → moneyshe.com/sipp

Capital at risk. The value of investments can go down as well as up. Tax treatment depends on individual circumstances and may change. This article is information, not personal financial advice.